Venture Debt Light: Growth without dilution of equity

No collaterals

Disbursement within 4 weeks

In-depth understanding of innovative business models

No equity kicker and without subordination requirement

Friendsurance

"Startups often get funding from business angels and venture capital funds, but rarely loans - certainly not in times of Corona. In the first quarter of 2020, investments in insurtechs halved worldwide. The fact that we got funding so quickly through creditshelf shows how compelling and solid our business model is."

Download whitepaper here

The Female Company

"I like the fact that creditshelf checks its investments very carefully at the beginning to see if financing is worthwhile and that I have the freedom to concentrate on building up the company afterwards instead of preparing monthly reports."

Targomo GmbH

"Thanks to the venture debt light loan from creditshelf, we were able to invest more in the further expansion of our sales and marketing team. The unsecured financing therefore came at exactly the right time to further accelerate our growth - thanks to an equally fast and smooth process!"

JOBMATCH.ME

"For us, creditshelf is an absolute added value due to its speed and we were impressed by the uncomplicated processing as well as the competent and very customer-oriented employees. At JOBMATCH.ME, we focused on profitability at a very early stage. This opened up financing opportunities beyond VC without further dilution. The capital now provided by creditshelf allows us to continue sustainable growth while keeping the momentum high, which is super important for us as a digital platform."

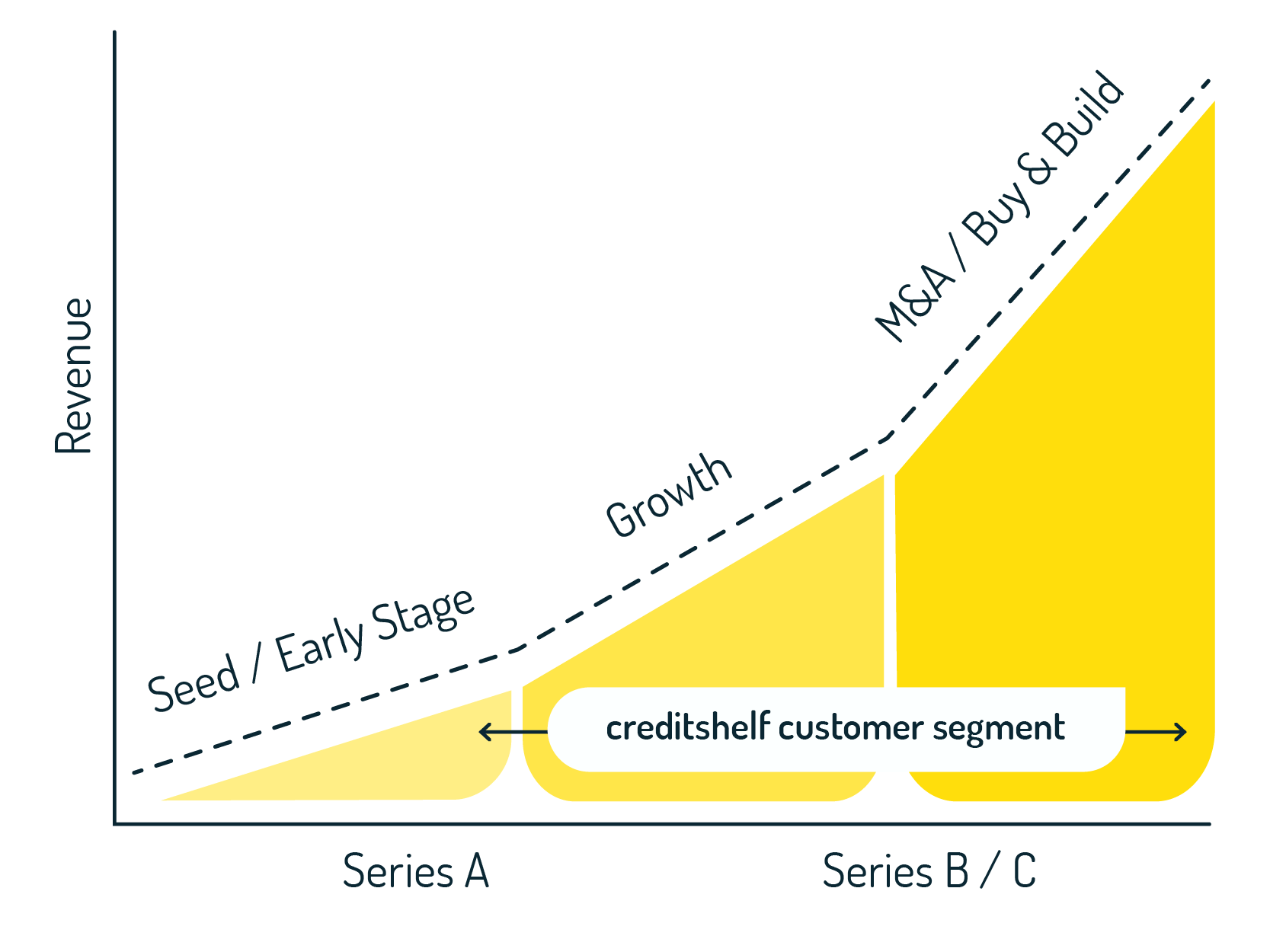

Especially for companies between the "start-up" phase, product-market fit and sustainable establishment, it is important to design the right financing mix.

With "Venture Debt Light", we enable tech growth companies to access debt capital at an early stage and offer a suitable supplement to equity financing. In doing so, we avoid dilution of company shares and are independent of the investment climate on the market. Our expertise lies in supporting companies from a seed / early stage or Series A round onwards, in which well-known investors are already involved.

The advantages of Venture Debt light are manifold and can vary depending on the market situation. For example, it can be used to circumvent down rounds, provide quick access to liquidity without valuation issues or avoid dilution at strategically important times. In addition, it may make sense to combine venture debt light with a smaller equity round to further drive the growth of the company. In any case, Venture Debt Light is a valuable financing component for emerging technology companies.

To differentiate: classic Venture Debt that comes with so-called equity kickers (warrants) will usually only delay dilution, not prevent it. Our Venture Debt Light does not dilute participating founders, existing investors or employees incentivised via ESOPs. We structure our Venture Debt Light with fixed, non-floating interest for the term of the loan in order to enable market –independent planning and thus security during our commitment – which in turn is in the interest of all investors, so that sufficient cash flow can be made available for future growth.

Conversely, it is clear that our venture debt light is not an equity round per se, but can be a sensible building block for combination with one - or (also simultaneously) serve to extend the runway, be used as a growth accelerator for e.g. marketing or further market development, or to pave the way for subsequent, more attractive equity rounds.

![]() Unsecured loans from EUR 100,000 to EUR 5 million

Unsecured loans from EUR 100,000 to EUR 5 million![]() Disbursement within 4 weeks

Disbursement within 4 weeks![]() Fast, easy and digital loan request

Fast, easy and digital loan request![]() Personal and binding service

Personal and binding service

Monthly rate:*

€

Duration:

months

Loan volume:

€

*Example for best credit rating category